1950s Buffett Investment - Union Street Railway

Union Street Railway was an early 1950's “cigar butt” investment of Buffett's

Introduction

Warren Buffett has spoken about the high returns he earned in the 1950s - especially in his pre-partnership days. Union Street Railway was one of these no-brainer, “cigar butt” investments he made during that time.

The Situation

While Buffett was working for Graham-Newman, he followed-up on a lead from Graham. Union Street Railway was a bus service that operated in Massachusetts (side fact: in an odd twist of fate, it operated in New Bedford, Massachusetts and counted Berkshire Hathaway’s Seabury Stanton as a director).

Union Street Railway was a classic Graham net-net, meaning it was selling at a large discount to current assets minus all liabilities, a conservative estimate of liquidation value.

Not only was it a net-net selling at a ~25% of book value, it had a few other features that made it an incredibly interesting and fairly “clean” investment:

Substantial portion of assets in cash plus highly liquid government securities

Was selling at 60-70% of cash+securities

Also had some other hidden cash assets (discussed later)

Nearly $0 of liabilities

Company repurchased ~16% of stock over last two years at large discounts to liquidation value

As Buffett described the situation in the “The Snowball”:

“[Union Street Railway] had a 116 buses and a little amusement park at one time. I started buying the stock because they had $800k in treasury bonds, a couple hundred thousand in cash…Call it a million dollars, about sixty dollars share. When I started buying it, the stock was selling around $30 or $35 per share.”

Why did the Situation Exist?

The (likely) two main reasons why this highly undervalued situation existed:

Incredibly Small, Highly Illiquid Stock

Union Street Railway’s market cap when Buffett was buying was ~$600k (around $6.9mm market cap in today’s dollars)

Very small company meant less investors looking at it and for those that found it, created a highly illiquid situation where buying enough stock was difficult. The company ran local ads itself in the local New Bedford paper in an attempt to repurchase its undervalued stock.

Buffett ran his own ads. Then he realized as a regulated utility he was able to obtain a list of the largest shareholders from the public-utility commission in Massachusetts. He utilized that list to find shareholders willing to sell their stock to him.

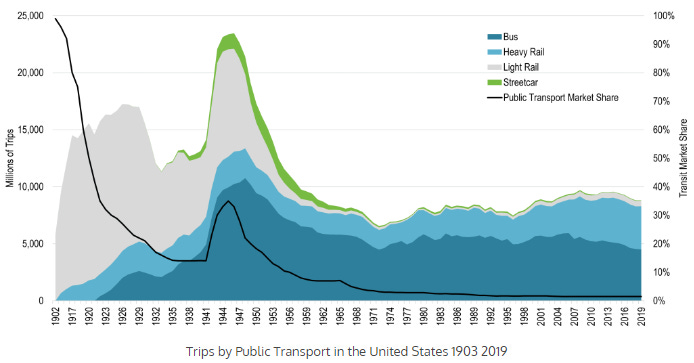

Declining Business

Bus usage, in terms of number of trips, began to decline post-WWII. Public transportation’s share of total transit was on a longer-term secular decline, accelerated by the automobile’s rise. However, during World War 2 a resurgence of public transportation occurred driven by austerity measures such as gas rationing. The World War 2 time period was also when bus usage increased dramatically and ultimately peaked.

In the post-WWII world, Union Street Railway saw passenger count drop drastically. They experienced a -49% decline in passengers from 1946-1953. Despite this, they managed to stay profitable up until 1953.

The $50/share Special Dividend

After purchasing the stock, Buffett went to see management on a weekend. At the end of the conversation, he learned Union Street Railway was planning a special dividend at a per share amount well above the current stock price.

"I got up at about four a.m. and drove up to New Bedford. Mark Duff was very nice, polite. Just as I was about ready to leave, he said, 'By the way, we've been thinking of having a return of capital distribution to shareholders.’ That meant they were going to give back the extra money. And I said, 'Oh, that's nice.' And then he said, Yes, and there's a provision you may not be aware of in the Massachusetts statutes on public utilities that you have to do it in multiples of the par value of the stock The stock had $25 par value, so that meant it would be paying out at least $25 per share. And I said, Well. That's a good start. Then he said, Bear in mind, we're thinking of using two units. ' That meant they were going to declare a fifty-dollar dividend on a stock that was selling at thirty-five or forty dollars at that time."

How the Investment Worked Out

After the special dividend, Union Street Railway traded at $20 per share at the end of 1956. Buffett still owned 576 shares (~$11.5k). A $20/share stock + $50/share special dividend equals $70/share of total value, equating to a likely >100% return over a relatively short period of time (unsure of Buffett’s exact original investment date).

“I got fifty bucks a shares, and I still owned stock in the place. And there was still value in it. The bus companies hid assets in these so-called special reserves and land and buildings and car barns where they kept the old streetcars.”

After the special dividend and accounting for some cash burn, the pro forma book value was likely in the ~$60-$80 per share region in 1956. With the stock trading at only $20 per share, substantial value was still there to be unlocked as Buffett mentions above.

Conclusion

No special insights were necessary to buy Union Street Railway stock. Although the company was likely in a long-term decline, extreme value existed above the stock price - and most of that value was in cash/securities. And, as an added kicker, if the other “hidden” assets were ever unlocked for the benefit of shareholders, all the better - but not necessary for a successful investment.

In fact, the most important factor was likely the hard work Buffett was willing to put in to track down shareholders in order to buy a material amount of stock. This seems to be one of Buffett’s most underrated characteristics: his ability/desire to go the extra mile for an investment (flipping thru 10,000+ pages of Moody’s Manuals, tracking down shareholders to acquire enough stock, etc.).

Ultimately, in Union Street Railway, Buffett was able to get one of the last “puffs” out of this cigar butt investment.

Disclosure: Please do your own due diligence before making any investment. None of my posts are investment advice. For full disclaimer, please click here. Feel free to contact me - I can be reached on this site or via my firm’s website here.