Group 1 Automotive (GPI)

Undervalued U.S. new car dealer with intelligent historical capital allocation focused on share repurchases

Summary

Group 1 Automotive (ticker: GPI 0.00%↑ ) is one of the largest new car auto dealers in the United States and also owns new car franchises in the United Kingdom. GPI operates in many states throughout the U.S. with a concentration in both the demographically favorable Sunbelt region (southern part of U.S., coast to coast), and the upper Northeast. GPI is the largest auto dealership in Texas, which has seen some of the highest population growth over the last decade.

As a new car dealership, GPI operates in an industry with a highly variable cost structure and its largest profit segment (parts and service) has limited cyclicality. The combination of these two factors allow dealerships to remain profitable even during deep recessions.

GPI has a simple capital allocation strategy of repurchasing stock at attractive valuations and acquiring additional dealerships. They have repurchased ~40% of their stock since 2013 and ~14% of their stock over the most recent prior three quarters, ending 2Q22. The new car dealership industry is highly fragmented with the public new car dealers only representing ~10% of new car sales. A long runway exists to continue to consolidate the industry, as has been occurring over the past few decades.

GPI currently trades at ~7-8x my estimate of normalized earnings and ~3.5x their current temporarily heightened earnings (driven by new car shortages). GPI’s elevated current earnings provide the extra benefit of additional excess cash to accelerate growth in value per share through either additional acquisitions or share repurchases. Even if you assume those heightened earnings go away tomorrow and only normalized earnings exist going forward, GPI’s stock could increase 2-3x over the next five years as additional cash generation occurs and the current undervaluation is corrected.

Operating in a durable and defensive industry, with minimal risks, and a cheap current valuation, GPI has great investment potential over the next few years.

Industry Overview

New car dealers are protected by strong franchise and state laws that effectively limit competition and in some cases operate as local monopolies of their brand. In many cases, these laws limit the manufacturers from opening a dealership of the same brand within a certain distance of an existing dealership. This dynamic is not all bad for the auto manufacturers, as it allows the dealers to more easily make the investments asked of them. More sales through a limited number of dealerships creates a stronger, more financially secure, dealership network, which benefits both parties.

New car dealers have four business lines: (1) new cars, (2) used cars, (3) parts and service, and (4) finance and insurance. To fully understand GPI, let’s walk through how the new car auto dealer industry works.

In normal economic environments, selling new cars is a low margin business, where dealers make a ~5-6% gross margin on the sale. However, those margins are worse – after considering indirect costs required to sell those new cars but not directly attributable to each individual new car sale (such as certain personnel and property costs) the margin is close to 0%.

Why sell a product that you make little to no money on? For the same reason Gillette sells it razors at no profit: large margins on the subsequent sales of razor blades from your now “built-in” customer base. New car dealers work with a similar business model, making money from new car sales in a variety of ways. First, when a new car is sold, a very high percentage of them are financed, either via a loan or a lease. When the dealer arranges the loan/lease for a customer, they are paid a commission by the finance company for the referral. Because there are no expenses attached to the commission it is a 100% margin business line for the auto dealer. Dealers also earn commissions when they sell products for insurance companies such as gap insurance.

Next, and most importantly, is the parts and service business where dealers average 50%+ margins. After a new car is sold it is typically on warranty with the manufacturer for three years. Meaning, that if any repair is required, and is covered by a warranty, the car’s manufacturer will pay their associated dealer for the cost of the repair. Once that new car is off warranty (or when they sell a used car), customers always have the option to service their car at an independent repair shop instead of a dealership. A certain percentage of customers will choose to go the non-dealership route, but certain customers will always feel more comfortable with a dealership servicing their vehicle versus the independent shop. Also, even when a customer chooses to service their vehicle from an independent repair shop, they still need parts to perform the repairs. Local auto dealers act as a supplier to many independent repair and collision shops, selling them the parts they need to complete their service work.

Better yet, the service business also has limited cyclicality, with consumer demand for vehicle servicing remaining fairly stable in all economic environments. Due to this, when new car sales decline dramatically in a recession, a dealership’s service business still generates lots of cash. The service business is one of the main reasons why the public auto dealers did not lose money even during the deep recession of 2008-2009.

The service business represents a disproportionate large amount of a dealer’s profits. Although each service transaction is a much smaller dollar amount than a car sale, since the margin on that service transaction can sometimes be 10x as profitable, it requires far fewer transaction to generate the same profits. To put that in numbers, in 2019 (using a non-COVID effected year), parts/service represented 13% of GPI’s revenues, but 45% of gross profits. Whereas, new car sales represented 52% of revenue but only 17% of gross profit. These facts really put into context the importance of the parts and service business, the largest contributor to an auto dealer’s gross profits.

Finally, each new car dealer operates a used car business at each dealership. Since the lowest-cost method to source used cars is from the consumer, new car dealers are especially well positioned to collect used vehicles in a variety of ways others cannot. The used car business is also less cyclical than new car sales. Industry-wide U.S. new car unit sales declined 40%+ in the Financial Crisis (from peak-to-trough), whereas used car unit sales only declined ~16%.

Variable Cost Business Model

Auto dealers, unlike auto manufacturers, operate with a highly variable cost business model. Compensation expense is by far the largest expense item in its cost structure, followed by advertising. Much of this compensation is paid to the dealer’s sales people, which comes in the form of small base compensation plus larger potential commissions. When sales decline, commissions automatically decline (less sales = less commissions). Dealer’s can also cut staff during a recession as they obviously need less sales people if they have less customers.

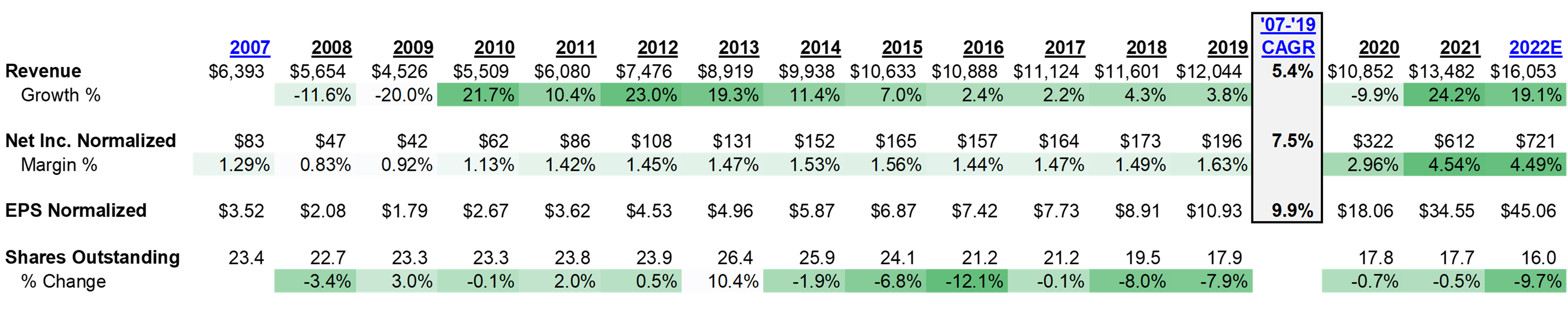

This dynamic combined with the ability to cut advertising expenses creates a the predominantly variable cost structure. For example, during the Financial Crisis, GPI’s revenues declined ~30% from 2007-2009. Despite this decline, operating margins only declined from 3.1% in 2007 to 2.8% in 2009. So, although revenues and profits both fell substantially during a very deep recession, GPI (and the other public dealers) still remained profitable. Profitability was only possible due to (1) the less cyclical service business being a large portion of a dealer’s profits, and (2) the ability to quickly/”automatically” pull costs out of the business once a recession begins.

Capital Allocation Strategy

After all this lead-in you are probably thinking, “that’s all great but why GPI over other public auto dealers then?” Although I think many of the U.S. new public auto dealers AN 0.00%↑ ABG 0.00%↑ LAD 0.00%↑ PAG 0.00%↑ are priced for high returns, the answer really is due to GPI’s capital allocation strategy, and relative valuation (discussed later in Valuation section below).

GPI operates with what seems to be the simplest capital allocation strategy of all the public dealers. GPI’s capital allocation strategy is simply (1) buy other new car dealers, (2) repurchase stock (bought back ~40% of company since 2013), and (3) pay a small dividend. Pre-COVID, this was the same strategy as many of the other public dealers. However, many are now seeking to buy more dealers and in a quicker timeframe, start standalone used car sites, start/buy their own captive finance companies, and are beginning to talk about venturing into selling products outside of cars such as RV’s and agricultural vehicles.

Nothing is necessarily wrong with any of these strategies, but they are all new strategies with no track record behind them. Also, outside of one or two of the public dealerships, most do not have a highly successful track record of success in simply acquiring other dealerships, which makes you question the potential success of their new ventures.

However, like any good operator, GPI has evaluated many of these ventures that the other public dealers are choosing to take on. On starting their own captive finance company, GPI noted on their 22Q2 earnings call, they are not interested – believe they have supportive finance partners currently and don’t want to add fixed costs to their business model. On standalone used car sites, mentioned as far back as 2015 how hard it is to make that model work, while discussing how three of the other public dealers failed in their attempts at starting standalone used-car sites.

GPI has intelligently realized that there is an opportunity in the used car space but they think they can utilize their existing infrastructure. In 2018, GPI introduced “Val-U-Line” used car offering which is just GPI retaining more of 6-10 year old cars instead of sending those to auction. First, this allows them to capture the margin they previously gave-up on those sales when offloading these types of cars in bulk to auctions. Also, GPI could not get the math to work on standalone used car stores so this was their version of it, allowing them to sell additional cars without additional fixed costs / infrastructure (along with their online selling portal discussed in next section). GPI believes this can also help increase the number of people coming to the dealership for service. They have stated they are not necessarily looking to sell cars to people far outside of their current markets. They want to retain their customers and gain future, higher margin, service work from them as well.

Final point on GPI’s capital allocation – they have shown the rare willingness to shrink their business when it makes sense. GPI purchased a Brazilian auto dealership group in 2013. Although they attempted to grow in Brazil, GPI ran into two main issues. One, they could not make additional acquisitions in Brazil it if they did not accept existing liabilities in deals related to tax/employees, and (2) the exchange rate kept deteriorating. Due to these factors, GPI divested their Brazilian operations in July 2022 for slightly less than $100mm (4-5% of current market cap) and can now re-deploy that capital towards better uses.

To sum it up, GPI is simple but focused. Although they have not been anywhere near as successful at making acquisitions as some of the other public dealers, they have repurchased ~40% of their stock since 2013 at attractive valuations. GPI’s simplicity and focus in capital allocation are very appealing, in addition to not pursuing a “conquer the world” strategy like others.

New Car Dealers Advantage in Used Car Business

GPI has coupled their Val-U-Line strategy selling older used cars with their recent online car selling website named AcceleRide in 2019. The other large public dealers are all introducing online sales, as they compete with Carvana and certain consumers desire to complete their car purchases online. Although Carvana has grown quickly (despite their recent struggles), the new car dealers do have certain advantages in the used car business over the online-only used dealers.

The four main ways dealers source used vehicles are from: (1) trade-ins, (2) off-lease returns, (3) direct consumer transactions, and (4) auctions. Options #1, #3, and #4 are available to used car lots and the Carvana-type CVNA 0.00%↑ online only used retailers but new vehicle dealers have two main competitive advantages in the used car business. First, off-lease returns are only available to new car dealers providing an additional source of used inventory that is less expensive than buying from an auction (and paying the associated auction and transportation fees). Second, whenever a customer buys a new car and trades in their used vehicle during the transaction, the new car dealership’s used vehicle inventory will increase. Used car lots and online used car dealers do not have this benefit. In a typical used-for-used transaction, the dealer’s inventory levels do not change. But, if a customer is buying a used car with no trade-in (e.g., first time car buyer), then their used inventory declines. By offering new cars, new car dealers benefit from customers exchanging their new car for a used car, which grows the dealer’s used vehicle inventory. Effectively you can think of this dynamic as a ratio or percentage all dealers have, indicating the replacement rate of their used car inventory. Since new car dealers have additional sources of used vehicles, their “replacement ratio” (my made-up term) should be higher than used-only competitors, which means they must go to the more costly auctions less often.

Carvana, and its peers, lack other advantages that new car dealers have. The second being new car dealers can make additional money, at high margins, from used car customers by servicing those vehicles post-sale, while also providing a “free” marketing opportunity for the dealer. And finally, and maybe most importantly, the dealers are selling these incremental online cars out of existing infrastructure. Slack capacity in both their service business and on their lots means new car dealers only incremental expense will be to build out the technology to sell online, which really just leverages their existing websites.

To sum it all up, versus the online start-ups such as Carvana (and even CarMax KMX 0.00%↑ ), new car dealers have advantages. They will be able to offer customers the same used vehicles, at better prices due to their lower sourcing costs, while also being able to make money from customers future servicing needs (which also provides a free marketing interaction with the dealership). Although Carvana may find a permanent spot among the used car dealers, large new car dealers with effective online portals, should be able to compete effectively against them.

Main Risks

New Management

Earl Hesterberg has served as GPI’s CEO since 2005. The Board recently announced that Hesterberg will retire at the end of 2022 and their current President of U.S. Operations, Daryl Kenningham, will become the new CEO. With any CEO change, the question is always how both the operational strategy and capital allocation strategy of a company change. With Kenningham as President of U.S. Operations since 2017, drastic operational changes seem unlikely.

The larger question is will Kenningham change GPI’s relatively “simple” capital allocation strategy and attempt a more aggressive approach that others in the industry are currently pursuing. With Hesterberg, who holds $43.5mm worth of GPI shares or 1.6% of the company, you knew his interests were strongly aligned with shareholders. He showed this by allocating capital to repurchasing shares at intelligent prices, while also not pursuing ventures that others in the industry were, noting many times that the “math did not work” on a specific venture, despite his peers eagerly pursuing these ventures. Kenningham currently owns $9mm or 0.3% of GPI, although that fiture will likely grow once CEO.

Kenningham’s career path is fairly similar to Hesterberg’s in that they have been in the automotive industry their entire careers and came up mainly in sales/marketing/operational roles. Despite this, Hesterberg has shown an ability to understand capital allocation mainly via the large share repurchases at intelligent valuation that have occurred over the past decade. Kenningham has been close witness of this but, of course, we’ll need to see what Kenningham does to truly understand how he will manage capital.

GPI does have a logical management incentive structure in-place that presumably will carry over to Kenningham. Both the short-term and long-term bonus/awards are increasingly focused on financial goals and are increasingly performance-vesting (as opposed to time-vesting). Long-term performance awards are based on ROIC and total shareholder return versus peers. With this incentive structure in-place, and the Compensation Committee of the Board trending toward more financial/performance focused awards, Kenningham should be properly incentivized to continue to manage the company in a shareholder-friendly manner.

Electric Vehicle Impact on Parts & Service Business

Electric vehicle’s (“EV’s”) engines contain less parts than the traditional internal combustion engine. Because of this, less parts fail or need service. This dynamic means auto dealer’s parts and service business will likely be negatively affected as EV’s are increasingly adopted. The size and timing of the impact will depend on many factors. On size of the impact, many in the industry have noted that although current EV’s require less service appointments, when they do enter a dealership for service, the amount of money spent by the customer is more than the traditional car. So there may be somewhat of a netting effect that occurs, with less transactions but higher transaction sizes.

On timing of the transition to EV’s, Mike Jackson, the former long-time CEO of AutoNation, said about a year ago that he expects by 2030 for ~20% of cars sold to be EV’s and ~7% of cars on the road to be EV’s. Obviously this could be drastically wrong, but it is also pretty accepted that the current U.S. electric infrastructure could not handle a full switch to EV’s today. Gradual consumer adoption combined with gradual U.S. infrastructure changes should mean this trend will not occur over night.

Also, outside of the potential EV shift, vehicles are becoming more complex. Each car is integrating more technology in the form of sensors, internal chips/computer, software, etc. Each of these make it more difficult for the do-it-yourself consumer looking to maintain/repair their own vehicle. At the same time, many small independent repair shops might not be able to make the required investment to provide service work on many of these advancing technologies, including EV’s. These factors are tailwinds towards increasing service work finding its way to the new car dealership, whose technicians are highly trained, and are larger companies with the financial resources to make the required investments for these new technologies.

Valuation

GPI’s valuation comes down to understanding normalized revenue and margins. Although this is true when valuing any company, the “normalized” piece is even more important given that auto dealer’s are currently earning outsized profits, driven by ongoing new car supply shortages. GPI has also acquired large dealerships since COVID began, divested their lower-margin Brazil operations, likely lowered their cost structure, and repurchased a large chunk of their shares. This creates a murky picture of future earnings and is probably the main reason why this opportunity exists.

Just want to note that by “normalized” I mean the profit potential GPI should make in an average year. Not a recessionary year, not a booming economy year, and definitely not a new car shortage year like 2022.

Let’s start with normalized revenue. A back-of-the-envelope way to estimate their normalized revenue is by looking at GPI’s historical fixed asset turnover. Essentially, how much revenue each dollar of fixed assets (e.g., property) generates. In the immediate years before the pandemic, GPI generated roughly $7.5 to $9 of revenue per dollar of net fixed assets. GPI’s current net fixed assets are around $2.0bn. Applying the $7.5-$9 range to $2bn implies $15bn-$18bn of normalized revenue, as compared to the ~$16bn of revenue GPI should generate in 2022. If at least some new and used car price inflation sticks around permanently, then the upper-end of the range is more likely.

The next piece is determining normalized margins. GPI operated around a 15% gross margin over the past decade. Auto dealers have experienced increasing penetration rates on their finance products over the years. Meaning, not only are auto dealers receiving commissions due to more customers financing or leasing their vehicle, but dealers are also receiving commissions from the increasing amount of additional service and insurance products being sold simultaneously. Due to higher penetration of these finance products, this means each car sold is generating more finance commission dollars (which are 100% gross margin sales).

Also, the pandemic likely caused a permanent shift in the way new cars are sold. Pre-2020, auto dealers dealt with near-permanently bloated inventory levels by discounting cars, with much of the discounting incentivized by the auto manufacturers. Sell a certain number of cars in a month and the manufacturers would pay the dealers a small “bonus” per car, if the dealer achieved those targets. This dynamic caused new car margins to decline over the past 10+ years. But once COVID shutdowns arrived in 2020, and the economy quickly re-opened thereafter, the auto dealers depleted their existing inventory as demand bounced back quickly. The auto manufacturers were not able to supply as many cars as pre-COVID due to the microchip shortage, driven mainly by consumers buying electronics for their new work-from-home lifestyle and inability to spend money on services (e.g., travel, lodging, etc.). A new car shortage resulted, lifting margins on new cars from ~5% pre-COVID, to 9-10% currently. The auto dealers obviously benefited by being able to sell closer to MSRP, while the auto manufacturers also realized that producing less supply, meant more pricing power. The auto manufacturers have mentioned they will seek to keep this dynamic in-place, in some respect, going forward and obviously the dealers agree.

The point of all this is that new car margins are likely to be higher in the future than they were for much of the past decade. These higher new car margins combined with the increased finance product penetration, means that normalized gross margins are probably higher than GPI’s historical 15%.

Then the question is what is GPI’s cost structure in terms of SG&A. Historically, GPI has had one of the more inefficient cost structures in the industry, operating at 73-75% SG&A as a percentage of gross profit. However, this figure included their now divested (as of July 2022) Brazilian unit which operated at ~90% SG&A/gross profit. Plus, management believes similar to coming out of the Financial Crisis, that they and others have figured out ways to be productive with less. With compensation expense being a dealer’s largest expense, lowering a dealer’s cost structure mainly means figuring out ways for each employee to be more productive. GPI management has mentioned they believe they permanently removed at least 400bps from SG&A/GP, implying a 69-71% range.

Finally, if auto dealers and manufacturers can keep inventory levels down versus pre-COVID, dealers will pay less in interest to hold their inventory and lowering their interest rate risk (more on the next section).

To end the long-winded explanation, this all sums up to a 2%-3% pre-tax margin, compared to the average ~2.4% pre-tax margin GPI managed from 2009-2020. Given all the potential positives to the margin structure of GPI, a 2-3% estimate for pre-tax margins is not outrageous. This implies ~$15-$25 per share of normalized earnings.

Final item to note is on the next five years of earnings. Even if these deployed earnings only generate dollar-for-dollar of additional market value, and the shortage-driven, $700mm+ of heightened earnings revert to normalized tomorrow, it is difficult to derive a scenario where a positive return for the investor does not occur at today’s ~$155 per share stock price.

Other Factors to Consider

Interest Rate Hedges

GPI management has also displayed their intelligence via the use of interest rate hedges on their floating rate debt. Auto dealers use floorplan financing to finance most of their inventory. Floorplan financing is typically floating rate debt, which means that utilizing the debt means less investor equity is required to be invested in inventory, but it does expose auto dealer’s to some interest rate risk. GPI’s management has realized this and has a unique feature the other auto dealers do not. GPI has interest rate swaps that have swapped a large portion of their debt from floating rates to fixed rates. As of June 30, 76% of GPI’s $2.8 billion in floorplan and other debt was fixed. Although the swaps expire on average around 2028, they do provide a large buffer against rising rates over the next few years.

Operational Strategy Focused on Parts & Service & Favorable Demographics

GPI, more than the other public dealers, seems to stress their operational focus on the parts and service business. They understand the importance of that segment, and the large profits it generates. Although not many unique operational strategies can be used in the service business, they have implemented a four-day workweek for their technicians. This allows the dealer to operate longer hours at each service bay and it allows technicians to have more consecutive days off (in exchange for longer hours each day). The expansion of open-hours, expands capacity for GPI’s service business, and it offers a wider variety of time availability to potential service customers, helping GPI better compete with the independents.

As noted previously, GPI is the largest auto dealer in Texas. Texas was third in population growth rate from 2010-2020 (+16% growth), and first in total population growth (+29.1mm residents). With no personal or corporate state income tax, along with its warm climate, Texas is attracting many additional residents and businesses. This means more people and cars on the road, which benefits every segment of GPI’s business, including their highly-important parts/service business.

Disclosure: I currently hold shares of Group 1 Automotive. I may buy more or sell my position at any time. Please do your own due diligence before making any investment. None of my posts are investment advice.

Thanks for the write up! What is your take on the quality of their UK business and how that added complexity of managing another geography impacts their growth and valuation relative to a US only dealer like ABG?