The Nifty Fifty & Business Quality

A quick article on the importance of business quality

Jeremy Siegel (Wharton Finance professor) wrote an article (link here) in 1998 that shows the importance of business quality for long-term investment performance. His article specifically discusses the Nifty Fifty.

As background, the Nifty Fifty was a group of ~50 U.S. stocks during the late-60’s/early-70’s. The group mainly consisted of large-cap, high-growth companies, with long records of dividend increases. They were often called “one decision stocks” as investors believed their prospects were so promising, you could buy and hold them forever.

Obviously with that investor mindset, things eventually were taken to an extreme. The valuations of the Nifty Fifty were ultimately pushed up to very high levels (~42x average P/E) and ultimately peaked in price around December 1972. Over the ensuing mid-70’s market declines, the Nifty Fifty declined dramatically along with the rest of the market. Many pointed to their decline as proving that the Nifty Fifty was just another bubble.

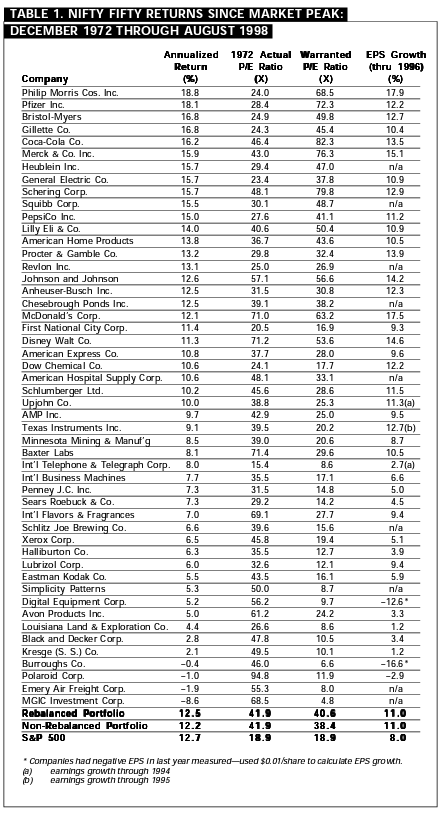

But Siegel argues there is more to the story. In his analysis (see table below), he shows the Nifty Fifty’s returns from their approximate peak in December 1972 to August 1998. Despite their much higher 41.9x average P/E at their peak, versus the S&P 500’s 18.9x, the Nifty Fifty’s stock performance roughly approximated that of the S&P 500’s (about 12-13% for each). The Nifty Fifty was able to achieve this mainly via higher earning growth over those 26 years (11% for average Nifty Fifty vs. 8% for S&P 500).

I think this stresses the importance of understanding two things in investment analysis: (1) the durability of a competitive advantage, and (2) the growth runway.

Using the Nifty Fifty list as an example, for most of those companies, assessing their competitive positions and growth runways over the next few decades would have been nearly impossible. To name a few, assessing IBM, Eli Lilly, or Xerox would have been tough in their high change industries. However, for a select few companies in lower change industries, it is conceivable that an investor could have achieved high confidence in the two stated categories.

I’d argue that three of the top five performers, Phillip Morris/Gillette/Coca-Cola, would be among the select few where confidence possibly could have been gained. All three had unbelievable brand power, leading to pricing power and an investor might have realized consumers were very likely to continue to smoke the same brand cigarette, shave with the same brand razor, and drink the same brand cola.

My final point is I’m not advocating paying 40x for every seemingly high quality business. Simply, value investors (myself included), tend to be leered in by statistical cheapness and are quick to disregard companies that are relatively highly valued on their current results. I would argue that investors need to pay just as much attention (if not more) to the durability and future growth potential of a business.

Just some quick thoughts on a Friday afternoon. And hopefully writing this continues to reinforce - in my value investor brain - the importance of business quality.