Thomasville Bancshares (THVB)

Top tier Georgia Bank with superior operating model

Summary

Thomasville Bancshares (OTC-listed: THVB) is a ~$410mm market cap bank located in Thomasville, Georgia. THVB’s superior management team created a bank that generates above average returns on assets via (1) scaled branches combined with an operational focus on “doing more with less”, and (2) a large trust division. But, most importantly, THVB has a common sense low-risk culture. Above average returns on assets combined with lower-than-average risk creates one of the better community banks in the U.S.

THVB currently trades at ~10x earnings. With this valuation, mid-to-high teen annualized returns are likely over a five-year investment period. For those willing to wait for higher returns, THVB makes for an interesting bank to watch whenever future forced selling occurs.

Low Risk Culture

(1) Low Credit Risk

THVB employees wear “multiple hats”, not doing any one job as they might at a traditional bank. In the typical bank, lending is typically separated into two functions: (1) a relationship manager who originates the loan and typically receives a commission, and (2) a credit officer who evaluates that loan and determines whether the loan is funded. Larger banks may have even more functions, meaning more costs and less speed.

Most relationship managers are compensated by their loan origination volume and not on how their originated loans perform. This dynamic can create bad incentives. THVB fixes this structure by making relationship managers also act as credit officers. They wear both hats and are compensated based on the long-term profitability of their originated loans. Additionally, with less channels to go thru, the loan process is much quicker than at a traditional bank – an important differentiator for many consumers and businesses. THVB has no pure managers at the bank - everyone is expected to be a decision maker.

What are the results of this lending structure? One only has to look at their losses during the 2008-2009 Financial Crisis to find out. THVB remained profitable throughout the Financial Crisis, despite Georgia being the state with the highest amount of bank failures. Not only did they remain profitable, but their lowest return on assets was ~1.0%, a figure that most banks strive to achieve in good times.

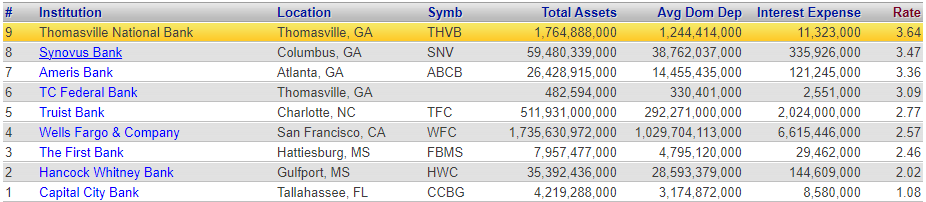

That extreme credit health remains today. THVB currently has very low nonperforming loans at 0.09% of loans. Relative to some of the banks they compete with, the figures look even better. Peers currently have nonperforming loans of 1.13% (see below).

The final item to note on credit losses is THVB is currently generating around 3.0% pre-tax pre-loan loss provision income to assets (“PTPP / assets”). With loans comprising 82% of THVB’s assets, that implies the bank could generate up to ~3.7% in loan losses (as % of assets) prior to losing money.

According to Federal Reserve data (see chart below), net charge-offs (i.e., loan losses) for community banks peaked at ~2.7% during the Financial Crisis. That means if THVB incurred a similar amount of losses, they would remain profitable due to their high PTPP / assets figures. The next banking crisis will surely be different than 2008-2009, but these figures give some frame of reference for what THVB can handle. And, with THVB’s heightened focus on risk, the loan losses are likely to be lower than the average 2008-2009 bank. THVB is an incredible, low-risk organization.

(2) Low Interest Rate Risk

THVB also avoided the interest rate risk that many banks gladly accepted in 2021 by investing/lending long-term at low rates. When deposit rates rose, securities values declined and margins compressed. THVB avoided these issues with the following philosophy (paraphrased from 2023 Annual Meeting):

Don’t lend long, since deposits are short-term

Do not chase yield and kept bond portfolio duration at ~1-year

Think when times are good that’s when you should put money into loss reserve

Be disciplined; don’t follow the herd

This disciplined / “don’t follow the herd” mentality can be seen in the percentage of their assets in long-term assets that re-price in >5 years. THVB operates with only ~9% long-term assets versus peers of ~33% (see below table).

Because most of their loan portfolio re-prices in <5 years, the timeframe most deposits will re-price in, their spread between loan/securities yields and deposit costs (net interest margin) experienced relative stability. Many other banks have seen much more significant changes (good and bad) in their net interest margins over the past five years, as interest rates changed dramatically.

Scaled Branches

THVB’s scaled branches hold more deposits than most banks in the U.S. THVB holds $381mm in deposits per branch, whereas their competitors hold an average ~$150mm.

The scale simply means THVB does more with less. Less branches mean less occupancy costs in the form of leases, maintenance, utilities, etc. Less branches also means less employees are required. Without extra branch costs, THVB operates with the lowest efficiency ratio among peers.

Due to their high cost efficiency, THVB can effectively pass on some of these efficiencies to depositors via higher deposit rates. As the below table shows, THVB has the highest interest-bearing deposit costs among its peers. While of course it would be better if they could generate/retain deposits at little-to-no cost, a win-win setup where THVB shares their efficiencies with customers is also a competitive advantage that few can provide their depositors without severely impacting profitability.

Thomasville depositors (where ~90% of their deposits are located) have undoubtedly valued their relationship with THVB as evidenced by their increasing deposit market share of the Thomasville MSA (steadily increased from ~39% to ~57% over the past decade).

Trust Revenue

In addition to THVB’s strong, pure banking franchise, they also operate a growing trust division named TNB Financial. Formed in 2001 has expanded over the years using various methods, including local acquisitions. They now manage $4+ billion in assets for clients and generate $16mm+ of revenue from this asset base.

Although this trust income will fluctuate as market valuations change, it provides (1) an additional income stream to offset any loan losses, fund growth, or go to shareholders, and (2) strengthens relationships with certain depositors who choose to have all of their banking/financial life done by both the bank and trust department (i.e., creates stickier clients/customers).

Return on Assets

Combining the (1) high-level of operational efficiencies, (2) trust revenue, and (3) the low-risk culture allow THVB to generate a return on assets well-above their competitors. In fact, their year-to-date return on assets (2.28%) is nearly double that of the 2nd place competitor (1.41%).

Compared to a larger list of all 132 Georgia banks with less than $2bn in assets, THVB ranks around the top 10% for return on assets and ranks as the #1 public bank in Georgia.

Valuation

Valuation of banks, over say a 5-year period, comes down to: (1) how much in assets will the bank have in the five years, (2) what return will be generated from those assets, and (3) how much in excess capital will be created over those five years that the bank does not need to retain to grow.

What will assets be in five years?

Over the last 5 years, THVB has grown assets by ~12% annualized. Over the past three years, they have grown at ~8% annually.

In the long-run banks, typically grow (via deposits) at a bit above nominal GDP growth (real GDP growth + inflation rate). If you assume THVB grows at a more conservative 5-6% over the next five years, they should have ~$2.3bn - $2.4bn in assets.

What will be the return on those assets?

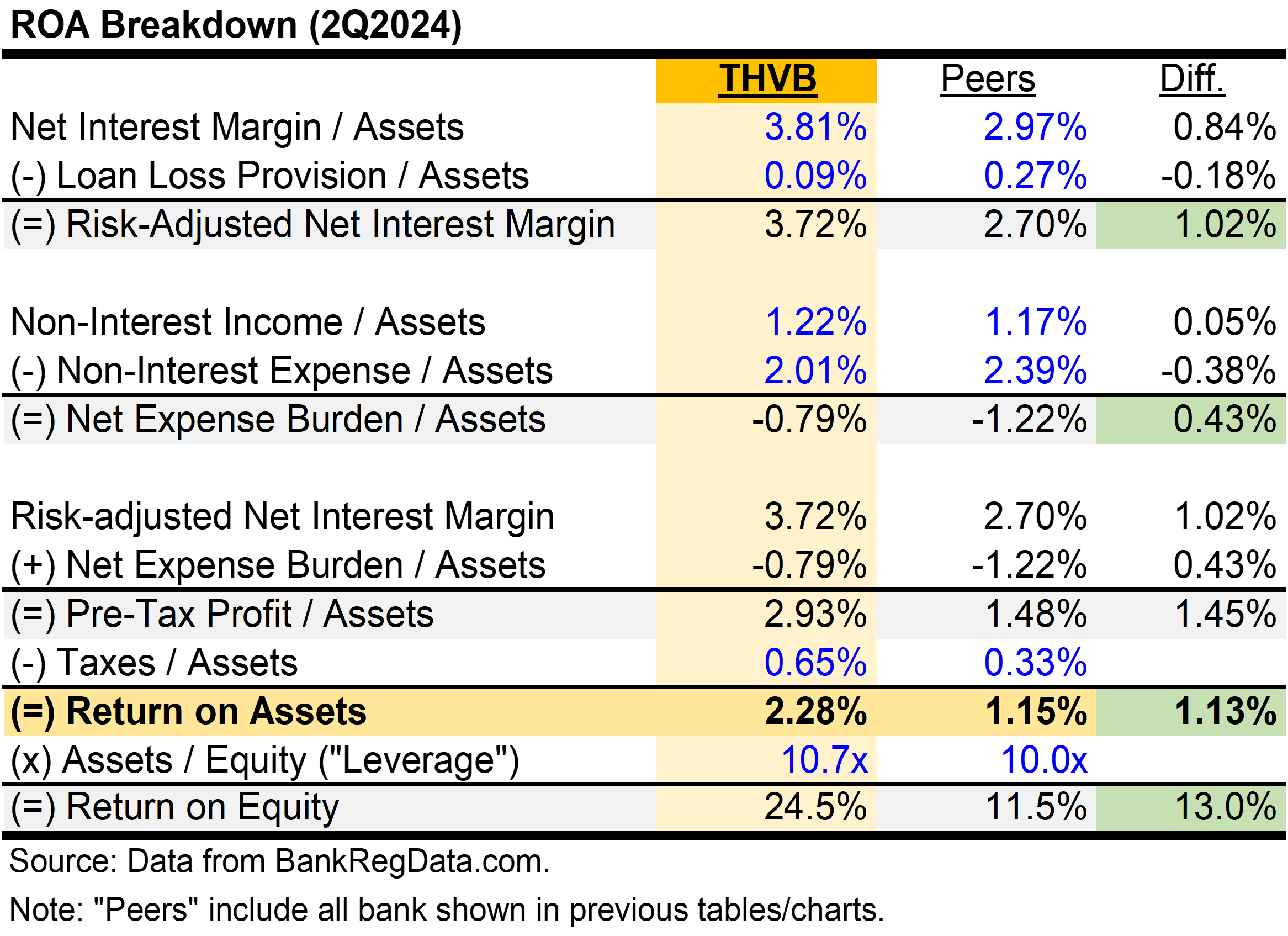

Above is a breakdown of THVB’s latest quarter’s return on assets (“ROA”). Going forward, with rates declining, THVB is likely to experience slight downward pressure on net interest margin. However, non-interest expense / assets should continue to decline as assets keep growing within THVB’s current infrastructure. A few other small pluses and minuses exist, but overall, I would expect future ROA to range between 2.0%-2.3% in normal economic environments.

If you combine the future asset range of $2.3-$2.4bn with 2.0%-2.3% return on those assets, you get, $46mm-$55mm in net income five years out.

THVB’s low risk means less cyclicality than the typical bank. High quality banks can trade in the 14-17x range, implying a roughly $640mm-$935bn valuation (or $100-$150 per share).

How much in excess capital generated over those five years?

Accounting for the capital required to fund growth and different economic environments, THVB likely generates $15-$25 per share in excess earnings (i.e., dividends and share repurchases) over the next five years.

Combining the valuation range with the excess earnings range results in $115-$175 per share of total value in five years. At a current $65 share price, that implies a 12%-22% IRR. An interesting valuation for one of the better community bank’s in the country but one to definitely pay attention to for higher future returns, if forced selling ever irrationally impacts the stock price.

Other Factors to Consider:

Insider Ownership

As of 2022 (latest ownership data I know of), ~27% of bank was owned by management and the board of directors.

The CEO, Stephen Cheney, and President, Charles Hodges, own a combined nearly 10% - strongly aligning interests with shareholders.

Share Repurchases

In January 2024, THVB announced a $5mm stock repurchase plan.

Although $5mm is a relatively small number for a $410mm market cap company, THVB does have a very illiquid stock, averaging only ~$108k of transactions per day over the last 30 days. The $5mm figure is likely close to the maximum they can in a year without affecting the stock price too much.

Disclosure: I currently hold shares of THVB for myself and others. I may buy more or sell my position at any time. Please do your own due diligence before making any investment. None of my posts are investment advice. For full disclaimer, please click here. Feel free to contact me - I can be reached on this site or via my firm’s website here.